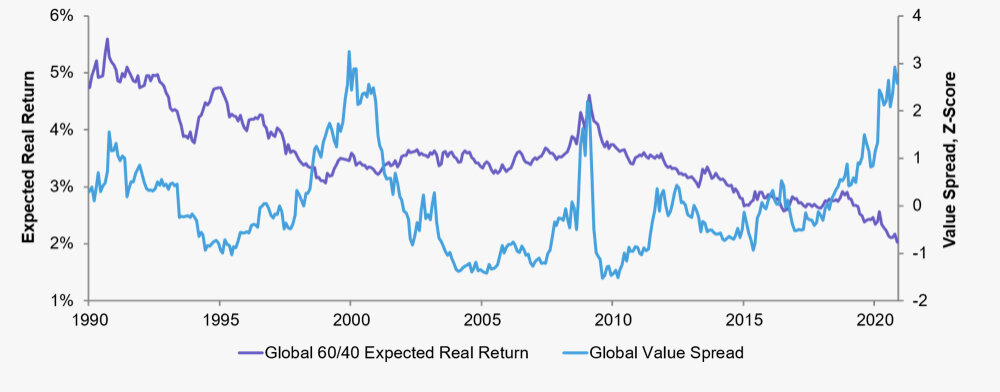

Value and factor investing from AQR

https://www.aqr.com/Insights/Perspectives/A-Gut-Punch

Value and factor investing from AQR

https://www.aqr.com/Insights/Perspectives/A-Gut-Punch

Note: I may have the ability to take on private wealth management clients in 2021 (fixed fee, 6K per year). Join the waitlist by emailing mccauleycapital@outlook.com.

So much of the investing advice you have heard over the years relates to creating an investing process that helps you overcome the natural pitfalls of human behavior. If an investment professional is telling you:

“to invest in index funds,” they might mean “most people are terrible at picking stocks, your investment returns will improve if you don’t pick individual stocks”

“to dollar-cost average into the market,” they might mean “make your investments free of emotions”

“automate your savings” might mean “humans often spend whatever cash is available to them (and sometimes more) if you don’t set money aside before you have a chance to spend it you won’t end up saving money at all”

This happens throughout life, people aren’t often as direct or articulate as might be ideal. However, when enough of this “translation” becomes commonplace the true messaging can get lost. In 2020, one key (often overlooked) principle drove returns - staying invested in times of uncertainty, turbulence, and even high-valuations. This extraordinary year was unique from an investing perspective, throughout the year one could have easily argued that the right thing to do was to sell stocks and move into “safer” positions, cash, bonds, gold, or Bitcoin (that’s a joke :)). The stock market started 2020 with high valuations relative to market history (more on this shortly). In March, the stock “fell off a cliff” without fears about the pandemic (and its potential impact on the economy). Yet, when we zoom out and look at market performance for the year. The S&P500 is up 13% (light green), NASDAQ up 40% (yellow) and the Dow is up 4% (blue).

And thus, in a year where there were all sorts of reasons to move away from equity investments… the stock market (I’ll focus on the S&P 500 from this point forward), did what it does most commonly - it returned somewhere between 10-20% annually (returns by year are shown below). Most experienced investors have learned this point over the years, there are several compiling reasons to sell your investments in any given year, but when you stay invested you will be rewarded handsomely.

Inquisitive minds will immediately understand the point above and jump to a more interesting question - “surely you aren’t telling to stay invested at these insane valuations, are you?” Well, it depends on your situation (many people with long time horizons and sounds strategy should stay the course), but I’m not saying you should completely disregard valuations either. As a value investor, I believe in buying undervalued assets and it’s hard to argue that US equities are undervalued at the moment.

Analysis from the Leuthold Group. Valuations from Feb 2000 vs. Nov 2020.

All the valuation factors “of the median stock in the S&P” are currently greater than they were at the peak of 2000. So, it’s easy to argue that current valuations aren’t sustainable and mean revision is coming, but that doesn’t mean that you should move to cash. High valuations in the US mean you should consider investing more of your capital in international markets, or focus more on a value strategy in the US (recommended reading here - Global Value: How to Spot Bubbles, Avoid Market Crashes, and Earn Big Returns in the Stock Market). Staying invested has rewarded investors in the past, and the future will be no different. Don’t let the true message get lost in translation, the bad habits created by trying to predict future returns will do more damage over the long-term than any possible savings they can provide in the short-term.

I can’t find the video of this, so you will have to trust my memory. Howard Marks is on CNBC and his segment follows some yahoo with a terrible business… as a transition between segments, the host asks Mr. Marks if he would ever invest in the “yahoo’s” business. And Mr. Marks says “for a price.”

Those three words are brilliant. The price you pay is what determines investment success. It’s reasonable to pay more for a great business with a sustainable competitive advantage then you would be to buy a dying business (no one argues that). But buying a great business at an expensive price is often a worse investment than buying a challenged business at a fantastic discount to its true (intrinsic) value. Vitaliy Katsnelson (@vitaliyk) clearly articulates the concept in the following tweets:

If you bought Disney in 1999 - which was a great company then - it would take 12 years to break even. $DIS another lesson -- > great company doesn't always equal great stock.https://t.co/z8IeIaBFfE pic.twitter.com/KyStvhja45

— Vitaliy Katsenelson (@vitaliyk) June 22, 2020

Cisco Systems - great company in 1999, still great company today. Folks who bought it in 1999 still waiting to break even.

— Vitaliy Katsenelson (@vitaliyk) June 10, 2020

Can you pay too much for a great company? Yes! pic.twitter.com/fqEC504Cov

Back to Howard Marks. Anytime you can spend reading Howard Marks is time well spent (I highly recommend his book “The Most Important Thing”). The following quotes help explain his “for a price” comment.

First-level things says, ‘It’s a good company; let’s buy the stock.’ Second-level thinking says ‘It’s a good company, but everyone thinks it’s a great company, and it’s not. So the stock’s overrated and overpriced, let’s sell.

First-level thinking says, ‘The outlook calls for low growth and rising inflation. Let’s dump our stocks.’ Second-level thinking says, ‘The outlook stinks, but everyone else is selling in a panic. Buy!’

Betting on the fastest horse rarely gives you the best odds of winning money, instead, you should bet on the horse whose odds are most undervalued (of course, you invest rather than waste money betting, right?). As an aside - In Colorado, where I live, sports betting was just legalized. If you want to better understand the difference between speculation and investing, bet on a few games. If you manage to stay rational, you will quickly see that betting requires too much luck to be a good investment (for the large majority of people). True investing, with a long-term strategy and clear process, has significantly better odds of success.

Yes, my wife loves “period pieces” ;)

I didn’t write a newsletter during the market downturn in March when the market was extremely volatile, but I did field calls and emails from 20ish friends, colleagues, and family members. Many people I talked to were concerned, and second-guessing their long-term investing strategies - some were looking for reasons to overreact. Overreacting and adjusting your investment strategies is the easy thing to do, the human brain is wired to react in a way the “protects” us, going back to our hunter and gatherer days. I only write this newsletter twice a year (instead of quarterly or weekly) because I find that (often) the more you talk/read/discuss the more you overreact. Looking back, the March drama looks like nothing but an emotional roller coaster.

Let’s look at a few simple examples with where real money was invested in balanced funds (US/International stocks, Muni bonds). The blue line is the invested amount and the green line is the account value. The accounts are roughly 80/20 stocks vs. bonds. The first example has a constant investment balance (i.e. you put 10k in the account 2 years ago and haven’t done anything sense).

Constant Investment Balance Account - The value of your account swings from 18% above to invested amount in February to 18% below the invested amount in March… but by June you are back to an 11% gain.

So your account value went from +18% to +11% in a few months? Who cares, right? You aren’t even planning to use this money for 20 years.

How does this look when you are actively adding funds (increasing balance) throughout the downturn? Worse!

Increasing Investment Balance Account - The value of your account swings from 15% above to invested amount in February, to 21% below the invested amount in March… but by June you are back to a 9% gain.

Why did the account where I’m adding money (approximately) every two weeks perform “worse” then the constant investment balance account? Howard Marks already told you why - the price you pay matters. I’m oversimplifying here to prove a point, but the reason the first account (constant balance account) outperformed the second account is because the first account invested funds at a better price (which led to better value, on average). The second account invested funds like clockwork at higher average prices and that ultimately hurt returns (it would be the opposite of the majority of my funds were invested during a period of undervaluation). That said, the second approach (investing at regular intervals has been recommended by me, and people smarter than me, many times) is a great approach for your average retirement or long-term savings account.

The key points here are:

Changing your perspective (often by shifting to a longer-term point of view) can make an unforgettable market crash feel like “nothing” in retrospect; and

The price you pay matters. Almost anything can be a good investment “for a price”

One additional note… I’m not saying all market downturns are “nothing” and you should expect to always have most of your money back a few months after a significant downturn (quite the opposite, in fact). I’m saying looking at investing performance over longer periods of time, without the feelings of panic and loss often reframe the story. In my opinion, one should be concerned about the current value of US stocks… because their valuations are near all-time highs. Depending on your situation that might not be the “for a price” that is right for you.

Happy 4th!

Coming in Q4: How to design compensation plans that are win-win and how designing them appropriately can increase engagement, retention, and profitability.

I wanted to use this space to tie-up a few odds and ends. I promise* the ideas here (although wide-ranging) will be valuable and I’m very hopeful that they will improve your ability to get more value in life - when you shop, invest, and sell goods. In the last section, I share a new visual to show underlying performance factors of my value fund.

First, I want to discuss residuals and residual value.

The Oxford Dictionary defines a residual as “remaining after the greater part or quantity has gone,” and;

Investopedia defines residual value as “the estimated value of a fixed asset at the end of its useful life.”

The term “residual” is a niche term not commonly used, please don’t get hung up on it (depreciation is likely a more commonly used term to describe a similar concept). The point I want to make is that how you think about the value of an asset at the end of its usefulness can totally change the cost and value. It can make expensive assets more affordable than cheap assets. If you have heard of residual values before, the term was likely used in relation to cars or trucks. I’ll start with a simple example in that space before I move to other asset categories. I believe Chevrolet Trucks advertised that they had the highest residual value heavily in the nineties. Yet today, it appears that the truck that holds its value the best over time is the Toyota Tacoma. Regardless, I’m guessing you have seen a graph similar to the ones below as you researched the pros and cons of buying a new or used car.

The actual numbers here aren’t super important, the trend is… I’ll walk through a really simple example using the graph above to illustrate a point. If you need a car for a year, how old of a car should you buy? Obviously, this depends on a number of complex factors, but if it’s just a decision based on the value lost - the car loses $1,607 of value from year 4 to year 5 ($10,719 - $9,112) vs. $6,250 from year 0 to year 1 ($25,000 - $18,750). As I mentioned, this concept seems fairly elementary (and well understood), I think the real power comes from applying it to areas where people forget about the residual value. Many people have made businesses to fill this void, why do you think people are offering to haul away your used appliances for free? They are gambling that the appliance you have decided has a residual value of zero (to you) has a residual value of greater than zero to someone else. Think about the deprecation curves above, as well, different products and different brands depreciate at different rates (think about a Toyota Tacoma vs. a Kia, Patagonia vs. Old Navy, or Nike vs. Unbranded Shoes). It is really valuable in life (and in investing) to understand how you can play the depreciation curve to your benefit (adjust the slope or understand how time influences the residual value). Time plays an important role here. The decision making process will be entirely different if you plan to use (or invest in) an asset for two years vs. ten years. Regardless, I hope you find the following examples thought-provoking:

You need a winter coat. You might buy a $500 coat. You might buy a $100 coat… have you considered buying a $500 coat that is 12 months old for $200, wearing it for two years and reselling it for $160? The third option isn’t for everyone (it likely isn’t for most people) but does provide the lowest cost per day to use the coat. You also get to use the much more expensive coat (which we assume is warmer, more comfortable, etc.). The third option seems like a huge benefit to me, because you are using your understanding of residual values and the depreciation curve to get the most premium product at the most affordable price.

***I understand I’m making some assumptions here… maybe you could sell the $100 coat for $60 two years later (I doubt it). Maybe you could get a friend to give you a coat for free. Maybe you wear the $100 coat for 30 years - that’s sweet. Maybe you don’t have $200 to spend on a coat. My point is to think about when option 3 might be ideal for you, so don’t get too hung up on the details.***

You need a car. You might buy a new car. You might buy a used car. What if you bought a used car that is scarce… like a late 60’s Mustang or an early 2000’s EuroVan. That choice might turn the depreciation curve into an appreciation curve. This is another example of approaching this challenge differently to get more value from the situation. The investing possibilities are numerous, anytime you acquire an asset you might be able to use the expected residual value to change the question in your favor.

You are buying a stock. You might buy the stock of a brand you like without understanding the financials (but please don’t). You might buy on a tip from a friend (but please don’t). What if buy because the stock was selling for $9 per share but it had $7 per share worth of assets (from cash to real estate to inventory, etc.). Maybe that turns the potential investment into something with very limited downside risk and huge upside potential.

You are buying exercise equipment or music equipment. You might buy new equipment… but you should probably buy used equipment. Exercise equipment and musical instruments are items that are frequently purchased new and lightly used. They are both great examples of items where the depreciation curve is (often) very steep in the first few months of use. I think you might be surprised by the number of bands that play with used equipment (random fact: the Beastie Boys bought the majority of their equipment for the Check Your Head tour from a small, weekly newspaper in L.A. called The Recycler).

A quick disclaimer: this isn’t easy. You have to know and understand the asset well, if you don’t (and in some cases, even if you do) you can lose money be misestimating the residual value. I hope you found this to be a worthy thought experiment though. I think residual value (depreciation curves) help explain a significant amount of day-to-day economics, like why renters that drive new, expensive cars are renters and not yet homeowners… so much of the monthly income is being eaten about the depreciation curve. I’ll close a graph of Jordan shoe prices over time to (hopefully demonstrate) how this concept can be used almost anywhere.

Resell trends of Jordans

Residual value is applicable everywhere

In my experience, understanding the key drivers of the performance of a mutual fund or ETF can be very difficult. If you hold an S&P 500 ETF that is weighted by market capitalization (this is typical) you are holding ownership rights to approximately 500 different companies, but you only see one performance figure for your fund. About 22% of the assets are concentrated in the ten largest companies (AAPL, MSFT, etc.). This makes it hard to determine the impact of any specific stock on your total return. There are some good tools out there to dig into this, which I plan to write about in future newsletters… For now, I want to share a visual I’ve created to help tell the story. Below is a breakdown of the performance of my value fund. The light lines show the individual performance of each stock held in the fund and the dark line shows the combined performance of the fund. Several factors make this visual possible (and hopefully valuable) - the fund is small (<10 holdings) and the holdings are equally weighted (a market-cap-weighted fund would tilt the overall results towards the performance of the largest companies). Let me know what you think of the graphic below because I hope to expand on this analysis in the future.

*good luck with this promise… I should say “I hope”

After almost 15 years or being fascinated by all things related to investing, I’m bored (which I imagine is how most people feel when they are forced to think about investing). There seems to be more quality content available today then ever before (brilliant authors, insights from fintwit, and so many high quality podcasts), yet I’m bored. Maybe being bored is a sign of growth, maybe it’s not, I honestly don’t know. Maybe the “waiting” for your returns to appear is the boring part, as Morgan Housel puts it:

90% of individual investing is "spend less than you make, diversify, wait." The other 10% is just trying to speed that up, for better or worse.

— Morgan Housel (@morganhousel) July 15, 2019

After all, I’ve invested 15 years reading and developing strategies that are right for me. I have strong (yet not set in stone) investing and personal finance beliefs, like:

Ben Graham’s teaching and investing style is more meaningful than Warren Buffett’s teachings and investing style (can’t wait for the criticism in this one)

Money can be spent wisely to increase happiness, but money isn’t the key to happiness

Luck plays a significant role in most things, including investing

Reading about human behavior is at least as important to investing success as reading about investing

Automate savings (pay yourself first)

Save more than you spend

Investing success has very little to do with intelligence

“Safe investments” are often riskier than “risky investments” over long time periods (look at purchasing power of t-bills vs. equities over a 40 year period)

Understanding mean revision is powerful

Jack Bogle is an investing hero who did an incredible amount of good for America’s “average” retiree

You should diversify your investments

Leverage is bad

Debt is (usually) bad

Simple investing strategies are usually better than complex ones

Buying undervalued assets and having patience will produce good results long-term

Minimize fees

Focus of returns after taxes

A quantitive approach can minimize behavior errors

Many agree that boredom is critical to the creative process. Is my next key insight just around the corner? I don’t know. Do the great investors of our time get bored? I imagine so.

Regardless, despite my boredom I found the following of interest in the last few months (which probably means they are of interest to you).

The death of value investing has been greatly exaggerated. https://t.co/p5mY45W2mT

— ValueStockGeek (@ValueStockGeek) May 29, 2019

I ran out of space, but this was savage. Not only did the Blockbuster execs sell all their stock, they bought Netflix stock! Not sure I know of any other example like this https://t.co/5ehyJ1Pfda

— modest proposal (@modestproposal1) July 27, 2019

The Value vs. Growth differential👇has never been so extreme, even during the Great Depression and the Dotcom bubble https://t.co/FWrpo4RpF6 pic.twitter.com/cs3wRYabXX

— ISABELNET (@ISABELNET_SA) June 6, 2019

"If you put $100 in to stocks and then save it for 70 years and invest it for 70 years, you’re going to have a fabulous amount of money. But myself, I’d rather be 20 years old with a few Euros in my pocket on the boulevards of Paris than be 90 years old with millions of dollars."

— Tren Griffin (@trengriffin) April 23, 2019

Michael Lewis found his podcasting voice in episode 2. This is exceptional! https://t.co/UTPmOEo0ZR

— K McCauley 🏔🏄🏻 (@kipmccauley) April 11, 2019

How Wealth Reduces Compassion

— K McCauley 🏔🏄🏻 (@kipmccauley) April 9, 2019

“Those who hold most of the power in this country.. come from privileged backgrounds.. most powerful among us may be the least likely to make decisions that help the needy & the poor. They may.. engage in unethical behavior.” https://t.co/wrLudgMQQE

Hey Alexa, turn it up. #IllCommunication pic.twitter.com/yxWi6iyjdX

— Beastie Boys (@beastieboys) May 31, 2019

"Because in the end, you won't remember the time you spent working in the office or mowing the lawn. Climb that goddamn mountain." - Jack Kerouac. pic.twitter.com/yO4tKAI1dG

— Appalachian Mtn Club (@AppMtnClub) July 10, 2019

I read The Wealthy Barber (which I recommend) recently and it changed (or reinforced) my thinking in a few key areas:

For most people, investing success is dependent on strong personal finance habits

The potentially more valuable point here is a broader one - choosing what you focus on is critically important. You won’t receive your desired outcome if you don’t understand the true drivers (inputs) of your desired outcome. If investing success is your desired outcome, but you don’t get the personal finance piece right (you have a negative savings rate) or you don’t control your emotions (you buy speculative “hot stocks”) you won’t achieve investing success.

You should be able to save more than $300k by implementing the tips in the book (with common sense investing)

Mr. Chilton recommends setting aside 10% of your salary for savings. Once you have set aside a decent amount (possibly enough to cover 3 to 6 months of expenses) in a standard savings account as an emergency fund, he recommends investing your 10% in low-cost equities (Wealthfront or Betterment are great options). This insight has the potential to be a game changer for your average family. When you run the numbers you see that a mid-career, middle-income family could expect their savings account to be worth well over $300k by the time they retire (in addition to their retirement accounts).

A dollar saved is two dollars earned

We have all heard “a penny saved is a penny earned” but that turns out to be incorrect. If you grab your most recent itemized paycheck you should be able to quickly prove this point. For each $100 you are paid, how much goes to Federal Taxes, State Taxes, Medicare, Retirement, Health Insurance Premiums, etc. It’s likely that somewhere between $30 and $50 of each $100 you make disappears with taxes and other deductions. So, each time you decide to spend a dollar think about how much you have to “earn” to pay for that expenditure… it’s close to two dollars. Understanding this helps to reframe the true cost of purchases.

I want to briefly focus on the first point because it can be applied broadly. In order to determine success, one has to define a successful outcome. We frequently talk about investing here, so let’s start by considering investing success as our ideal outcome. If investing success is your goal what is the first thing you should focus on to achieve your goal? It’s certainly not asset allocation and it’s probably not even taxes or fees (this assumes you aren’t already independently wealthy). In order to achieve investing success, you are going to have to create money to invest… which is dependent on your personal finance habits. To farther illustrate this point, I’ve leveraged the USDA original food pyramid (which was used from 1992 - 2005). I remember this vividly from my childhood; it seemed to strongly imply that “bread, cereal, rice, and pasta” were good and the foundation of a healthy diet. While fats and oils were bad (there is significant controversy about how these recommendations were made by the USDA and what role the wealthy companies in the food industry played in crafting these recommendations). For our purposes, let’s disregard if the food pyramid is right and focus on the story it tells. If we tried to make a “food pyramid” for investing success it might look like the second image below.

The USDA's original food pyramid, from 1992 to 2005.

Simple “investing pyramid”

I hope our “investing pyramid” illustrates the appropriate story. Your natural tendency is first to seek advice on your asset allocation strategies, but when you do that you are focusing on the wrong thing. Before you worry about asset allocations, set your foundation with strong personal finance strategies that enable you to invest more money, minimize your taxes and fees, etc.

When we apply this idea broadly, to areas where our focus may be misguided, I think of the following:

We often focus on: Investing (especially Asset Allocation & “Hot Stocks”), but we should focus on Personal Finance and Savings

We often focus on Money, but we should focus on Happiness, Well-being

We often focus on Tasks, but we should focus on Relationships

We often focus on Caffeine, but we should focus on Sleep

We often focus on Ourselves, but we should focus on Family and Friends

We often focus on Possessions, but we should focus on Experiences

We often focus on Our wants, but we should focus on Our neighbor’s needs that aren’t being met (by volunteering or giving back)

Regardless, you should read The Wealthy Barber, it’s enjoyable and it will reduce your stress levels.

I always wanted to put together a list of recommendations for my readers, because so much of what I read and listen to is curated by my friends, family and coworkers. I truly appreciate recommendations from people I respect so I wanted to return the favor.

The foundational investing book everyone should read. It will change you understanding of the costs of not leveraging a long-term strategy that includes compounding. If you want to read it and you are in Colorado let me know, I have about 10 copies in my library that I loan out to friends.

Endure collects and explains a significant about of research around the performance of humans during all types of endurance events (hiking in Antarctic, climbing Everest, running crazy distances), it’s exceptionally interesting. “Makes the case that we’re actually underestimating our potential, and reveals how we can all surpass our perceived physical limits.” - Adam Grant

A surprisingly great read about Edward Thorp, the greatest investor you have never heard of. It’s an true story of the card-counting mathematics professor who taught many “how to beat the dealer” and became one the first of the great quantitative investors, crushing the market in nearly all conditions.

When Michael Mauboussin recommends a book I take note. It promises to provide a toolkit to help us better leverage data and analytics to our advantage.

My favorite investing strategy comes from the "father of value investing," Benjamin Graham. It works for me because it fits my temperament and personality; and it's logical for me (in part, because I've added my own "safety net" to the approach). It's probably not the ideal investment strategy for you (Jim O'Shaughnessy had a few well written tweets on this recently: 1, 2) but it has been the foundation of my investment approach for over a decade. In this quarter's newsletter, I review the performance of this strategy and revisit a few of my favorite parts of Ben Graham's classic book The Intelligent Investor.

First, the three year performance figures (more about this approach here). I'm planning a future post about how I leverage global value stocks (GVAL) in this strategy when the US market is overvalued. Obviously, I'm quite happy with this performance, but I don't expect the good times to continue forever (even the best strategies underperform the market about 30% of the time).

Second, let’s review a few nuggets of wisdom from The Intelligent Investor. My book is full of highlights, and I wanted to limit the length of this post so I limited myself to nine quotes.

“Several years ago Ben Graham, then almost eighty, expressed to a friend the thought that he hoped every day to do “something foolish, something creative and something generous.”

This is a fun quote from the start of the book... when is the last time you did “something foolish, something creative and something generous” in a day? I think of Mr. Graham as an analytical type so it really strikes me that he recommends being foolish and creative on a daily basis.

“The defensive investor must confine himself to the shares of important companies with a long record of profitable operations and in strong financial condition.”

Graham consistently discusses the value of the long-term track record. In my experience, it's difficult to find companies that have a ten year history free of share dilution, dividend cuts, excess debt, etc. Companies with strong historical metrics tend to offer downside protection.

“The third is the device of “dollar-cost averaging,” which means simply that the practitioner invests in common stocks the same number of dollars each month or each quarter. In this way he buys more shares when the market is low than when it is high, and he is likely to end up with a satisfactory overall price for all his holdings.”

Graham (and basically all intelligent investors) recommend dollar-cost averaging.

"The rate of return sought should be dependent, rather, on the amount of intelligent effort the investor is willing and able to bring to bear on his task. The minimum return goes to our passive investor, who wants both safety and freedom from concern. The maximum return would be realized by the alert and enterprising investor who exercises maximum intelligence and skill.”

A greater return is available to those who are willing to "work" for it. However, if you don't have the right temperament, skills and patience you are best severed as a passive investor.

"The Basic Problem of Bond-Stock Allocation We have already outlined in briefest form the portfolio policy of the defensive investor.* He should divide his funds between high-grade bonds and high-grade common stocks. We have suggested as a fundamental guiding rule that the investor should never have less than 25% or more than 75% of his funds in common stocks, with a consequent inverse range of between 75% and 25% in bonds. There is an implication here that the standard division should be an equal one, or 50–50, between the two major investment mediums. According to tradition the sound reason for increasing the percentage in common stocks would be the appearance of the “bargain price” levels created in a protracted bear market. Conversely, sound procedure would call for reducing the common-stock component below 50% when in the judgment of the investor the market level has become dangerously high."

Graham emphasized owning high-grade bonds and holding between 25% - 75% of your portfolio in bonds.

“Nonetheless we are convinced that our 50–50 version of this approach makes good sense for the defensive investor. It is extremely simple; it aims unquestionably in the right direction; it gives the follower the feeling that he is at least making some moves in response to market developments; most important of all, it will restrain him from being drawn more and more heavily into common stocks as the market rises to more and more dangerous heights.”

Graham recommends a 50/50 mix of stock and bonds for the defensive investor.

"A caution is needed here. A stock does not become a sound investment merely because it can be bought at close to its asset value. The investor should demand, in addition, a satisfactory ratio of earnings to price, a sufficiently strong financial position, and the prospect that its earnings will at least be maintained over the years. This may appear like demanding a lot from a modestly priced stock, but the prescription is not hard to fill under all but dangerously high market conditions.”

Throughout the book, Graham frequently emphasizes caution and defensiveness. It's clear to me that Graham's experiences during the great depression shaped his thinking. Every time I review The Intelligent Investor this stands out to me, it's almost always a good time to wonder: is my current investment strategy too aggressive?

"Let us close this section with something in the nature of a parable. Imagine that in some private business you own a small share that cost you $1,000. One of your partners, named Mr. Market, is very obliging indeed. Every day he tells you what he thinks your interest is worth and furthermore offers either to buy you out or to sell you an additional interest on that basis. Sometimes his idea of value appears plausible and justified by business developments and prospects as you know them. Often, on the other hand, Mr. Market lets his enthusiasm or his fears run away with him, and the value he proposes seems to you a little short of silly. If you are a prudent investor or a sensible businessman, will you let Mr. Market’s daily communication determine your view of the value of a $1,000 interest in the enterprise? Only in case you agree with him, or in case you want to trade with him. You may be happy to sell out to him when he quotes you a ridiculously high price, and equally happy to buy from him when his price is low. But the rest of the time you will be wiser to form your own ideas of the value of your holdings, based on full reports from the company about its operations and financial position."

Mr. Graham created "Mr. Market" to explain how irrational the crowds that drive market prices can be. Understanding that prices don't always reflect true value is key to understanding how one can create a strategy to outperform the market.

"The most realistic distinction between the investor and the speculator is found in their attitude toward stock-market movements. The speculator’s primary interest lies in anticipating and profiting from market fluctuations. The investor’s primary interest lies in acquiring and holding suitable securities at suitable prices."

Graham makes a clear distinction between the "speculator" and the "investor." I'd argue that the majority of individuals that own stock act as market speculators and not true investors.

Recommended reading.

https://www.l2inc.com/daily-insights/no-mercy-no-malice/happiness-the-gorilla

Let’s start with a question: Are you an above-average driver?

Chances are, about 85% of you answered yes. This means that 35% percent of the population answered this question incorrectly. Yet, even knowing that information, you are likely thinking to yourself “who are these people that are overconfident of their driving ability, because it’s surely not me.”

I mention this because, in past newsletters, we have discussed how the typical investor underperforms the market (link). I’m guessing you read that information and thought… other people underperform the market, not me (just like other people are below average drivers, not me). I have a challenge to see if you’re right. I’ve compiled historical returns from various mutual funds. I’ll provide the past performance figures and you pick the one that you expect to perform best (for now, just assume that I have done the research on these funds and they can be considered a wise investment).

Which fund did you pick? My guess is 90% of you picked B, E or I (highlighted below). In the next table, I show the performance of each of these funds for the ten years following the date that you made your selection.

At this point, many of you probably have buyer’s remorse. Funds B, E and I didn’t perform as well as you might have expected them to. If you could select again, which funds would you select? Funds A, D and H seem ideal given perfect hindsight. Yet personally, I never would have picked those funds, especially not A or D because they performed so poorly in the past.

This exercise is designed to explain a concept common in investing (and life) called mean reversion. Investopedia defines mean reversion as “the assumption that a stock's price will tend to move to the average price over time” and you can see this happening in the above example. Periods of underperformance are often followed by outperformance and vis-versa. I’ve include a brief three-minute video with some additional background on mean reversion, below.

Now to illustrate this point, I took a few liberties with the facts in my example above. The returns I used were actually provided were decade long returns for large stocks (via James O'Shaughnessy). Here is what the full chart looks like…

A graph helps to illustrate the up and down (mean reversion like) nature of stocks since 1910.

In order to clarify this concept, let’s discuss an example of mean reversion that doesn’t involve investing. Assume I play basketball and I’ve made 30% of the first one thousand three point shots I’ve attempted (shots 1 – 1000). Over the next one hundred three point shots I take (shots 1000 to 1100) I only make 17% of them. In the subsequent one hundred three point shots I attempt (shots 1100 to 1200), would you expect me to:

We know if I take a large number of shots I should shoot 30%. In our most recent smaller sample (of 100 shots) I only shot 17%. Therefore, I’d suggest I’m most likely to shoot >30% over the next one hundred shots (which would push my average shooting percentage closer to 30%, thus reverting to the mean). Of course, there are no guarentees what will happen in the next hundred shots, any range of outcomes is possible.

So now that we have all had a quick introduction to mean reversion – let’s try this again. The following graph is from a value focused fund I manage. Between August 2015 and August 2016 it outperformed the S&P 500 (blue line). Can you guess what happened next?

From Aug 2016 and Aug 2017 it underperformed the S&P 500 (reverted to the mean).

Finally, let’s look at the performance of the fund since inception. Periods of underperformance (highlighted by triangles) made outperformance (from that point in time) more likely. Similarly, periods of outperformance (highlighted by circles) were often followed by periods of underperformance.

The takeaway from this post shouldn’t be a hard and fast rule – not everything reverts to the mean. Great companies, great funds and great housing markets can outperform their benchmarks for significant periods… and some companies (or even stock markets) tumble down all the way to zero. Yet, I’ve found using the concept of mean reversion to frame future expectations as a helpful tool. Hopefully you will too.

We are looking for an editor to edit posts like this... Interested? Email mccauleycapital@outlook.com

Recommended reading: A thought provoking post from Patrick O’Shaughnessy on Growth without Goals.

I enjoyed this read from Research Affiliates...